The Bear Market is Back, Will it Hibernate Soon?

After a summer rally, volatility is back in full swing. 2022 has challenged investors’ patience as almost every investment has had negative returns, with the exception of commodities, the US dollar, and cash.

What’s Happening?

It appears investors and markets have run out of patience and just want to be done with this bear market and the recession talk. Instead, they are hoping that inflation has peaked and the Federal Reserve (Fed) will soon start cutting rates just as it began raising them. This disconnect is one of the reasons why the markets have floundered this year.

Since Fed Chair Jerome Powell announced the first interest rate hike in March 2022, the stock market has hoped that rate hikes would be short-lived. This was built on the assumption that the toll from rate hikes would soon lead to an economic slowdown and that inflation would sharply retreat in the same fashion as it appeared. In fact, after each of the rate hikes in 2022, markets were disappointed when the Fed appeared more hawkish and failed to slow its path of rate hikes, and the subsequent rally in the S&P 500 index failed.

What’s Next?

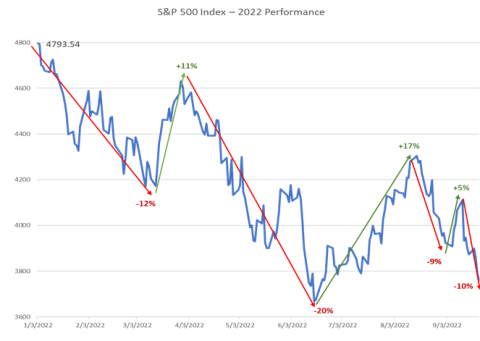

The million-dollar question is whether the Fed will be able to tame inflation without causing a recession. The US economy has experienced back-to-back quarters of negative growth for the first half of 2022, a sign of a technical recession. However, we believe a true recession has not yet begun. History tells us, if the economy does experience a recession, markets could fall further. Bear markets accompanied by a recession tend to be steeper than those without an economic downturn. Since 1946, the average decline for a bear market associated with a recession was 35.8% versus 27.9% on average without a recession.1 At its low point earlier in June, the S&P 500 had dropped roughly 24% from its high on January 3. While the markets have inched closer to historical averages without a recession, the bad news is there could be further pain should a recession follow.

While preparing for challenging markets and recessions is never easy, it is also important to understand that today’s challenges are not the same as those seen during the past two recessions. The recession in 2020 was triggered by a global pandemic but ended quickly as the economy re-opened. The financial crisis in 2008-2009 was a financial crisis, which resulted in a deeper and longer-lasting recession. The current environment on the other hand is a slow deterioration in the economy caused by the Fed’s fight against inflation. Neither kind of economic challenge — the deep, sharp declines or the long gradually developing ones — is easy but, at least this time around, we have the foresight to plan appropriately.

What is an Investor to do?

Bear markets, while painful, do not last forever and pale in comparison to bull markets both in length and size of gains. Looking at the history of the S&P 500 since 1942, the average bull market lasted 4.4 years with an average cumulative gain of 154.9% while the average bear market (decline of 20% from peak) lasted 11.3 months with an average cumulative loss of -32.1%.2

Conclusion

Bear markets test investors’ emotional strength to stick to their long-term plans. The best advice during these periods is to stay calm and ensure we avoid emotional decisions, given how costly its impact can be on investors’ portfolios. Finally, drawing on the old proverb, it is darkest before dawn. When market volatility seems to have no end; it’s important to have a long-term perspective and make sure the portfolio is designed to be balanced enough to benefit from periods of growth, while being resilient during these inevitable periods of volatility.

- FactSet. Data as of 1/3/2022-9/23/2022

- First Trust. History of Bull and Bear Markets. Data as of 6/30/2022

- Wells Fargo Investment Institute. The perils of trying to time volatile markets

AssetMark, Inc.

1655 Grant Street

10th Floor

Concord, CA 94520-2445

800-664-5345

IMPORTANT INFORMATION

This is for informational purposes only, is not a solicitation, and should not be considered investment, legal or tax advice. The information in this report has been drawn from sources believed to be reliable, but its accuracy is not guaranteed, and is subject to change. Investors seeking more information should contact their financial advisor. Financial advisors may seek more information by contacting AssetMark at 800-664-5345.

Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss. Actual client results will vary based on investment selection, timing, market conditions, and tax situation. It is not possible to invest directly in an index. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Index performance assumes the reinvestment of dividends.

Investments in equities, bonds, options, and other securities, whether held individually or through mutual funds and exchange traded funds, can decline significantly in response to adverse market conditions, company-specific events, changes in exchange rates, and domestic, international, economic, and political developments.

Bloomberg® and the referenced Bloomberg Index are service marks of Bloomberg Finance L.P. and its affiliates, (collectively, “Bloomberg”) and are used under license. Bloomberg does not approve or endorse this material, nor guarantees the accuracy or completeness of any information herein. Bloomberg and AssetMark, Inc. are separate and unaffiliated companies.

AssetMark, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission.

©2022 AssetMark, Inc. All rights reserved.

104766 | C22-19217| 09/2022 | EXP 09/30/2024